3QFY2018 Result Update | Banking

February 15, 2018

ICICI Bank

BUY

CMP

`328

Performance Highlights

Target Price

`416

Particulars (` cr)

3QFY18

2QFY18

% chg (qoq) 3QFY17

% chg (yoy)

Investment Period

12 Months

NII

5,705

5,709

(0.1)

5,364

6.4

Pre-prov. profit

5,057

6,986

(27.6)

5,524

(8.5)

Stock Info

PAT

1,650

2,058

(19.8)

2,442

(32.4)

Sector

Banking

Source: Company, Angel Research

Market Cap (` cr)

2,11,094

ICICI Bank PAT for the 3QFY18 declined 32% yoy to `1,650cr affected by higher

Beta

1.6

provision and weak other income. Key positive during the quarter was the

52 Week High / Low

365.7/241

divergence with RBI as FY17 NPA was lower than the threshold required for

Avg. Daily Volume

11,43,723

disclosure.

Face Value (`)

2

Healthy growth in retail advances

BSE Sensex

34,300

During 3QFY18, the bank’s advances grew by 10.5% yoy (4.7% qoq), aided by

Nifty

10,546

Reuters Code

ICBK.NS

healthy retail loan book growth of 22.4% yoy. The main drivers leading to the

Bloomberg Code

ICICIBC@IN

growth in the retail loan book were Personal loans and credit card loan, which

grew by 44.7% and 26.9% yoy respectively. Retail contribution to total loans

increased to 54% as compared to 49% in the corresponding quarter of the

Shareholding Pattern (%)

previous year. The corporate loan book grew 4.6% yoy (3.5% qoq).

Promoters

NA

Deposits growth was modest at 11% yoy, while CASA deposits saw a growth of

MF / Banks / Indian Fls

42.1

12.4% yoy, resulting in improvement in CASA ratio by 0.52bp yoy to 50.4%. The

Reported NIM fell by 13bp qoq to 3.14%, with domestic NIM at 3.53% as

FII / NRIs / OCBs

47.3

compared to 3.57% in 2QFY18. The Compression in NIM largely owing to

Indian Public / Others

10.6

international operation.

On the asset quality front, the bank witnessed slippages during the quarter to the

Abs. (%)

3m 1yr

3yr

tune of `4,380cr (annualized slippage ratio at 3.5% Vs 3.9 in Q2FY18). The Gross

NPA ratio fell 5bp sequentially to 7.82%, whereas the Net NPA declined 23bp qoq

Sensex

3.7

20.6

17.0

to 4.2%. In Q4FY18 bank has to take additional provision for NCLT-2, current

ICICI Bank

4.2

28.3

5.2

provision held at 36.4% whereas RBI requirement is 50%. Total exposure wherein

stands at `11,400cr spread over 16 accounts.

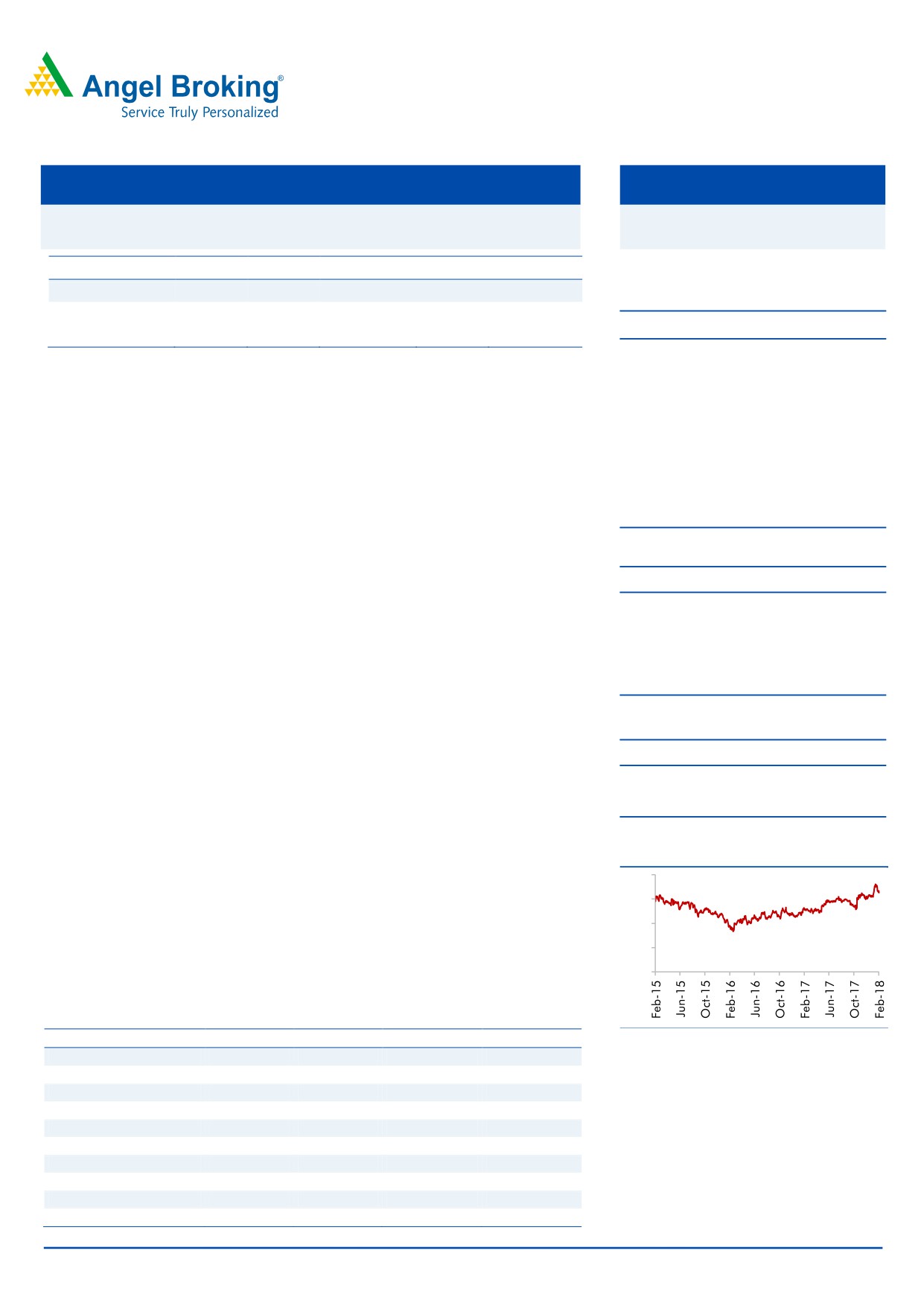

3-year price chart

Outlook & Valuation: At the current market price, the bank’s core banking

400

business (after adjusting value of subsidiaries) is trading at 1.1x FY20E ABV. We

300

believe strength of liability franchise (CASA-50%), shift in loan mix towards retail

200

assets and better rated companies, Strong capitalization (tier I of 14.6%), and

100

steady improvement in stress loan and going forward quick resolution under IBC

0

would be the key trigger for multiple expansion. We recommend a Buy rating on

the stock, with a target price of `416.

Key financials (Standalone)

Source: Company, Angel Research

Y/E March (` cr)

FY2017

FY2018E

FY2019E

FY2012E

NII

21,738

22,992

26,390

30,871

% chg

2

6

15

17

Net profit

9,802

7,726

9,382

14,185

% chg

0.8

(21.2)

21.4

51

NIM (%)

3.2

3.1

3.2

3.2

EPS (`)

15

12

15

22

P/E (x)

22

27

22

15

Jaikishan Parmar

P/ABV (x)

3

2

2

2

022 - 39357600 Ext: 6810

RoA (%)

1.3

1.0

1.0

1.4

RoE (%)

10

8

9

12

Source: Company, Angel Research; Note: CMP as of February 15, 2018

Please refer to important disclosures at the end of this report

1

ICICI Bank | Q3FY2018 Result Update

Exhibit 1: 3QFY2018 performance (Standalone)

Particulars (` cr)

2QFY17

3QFY17

4QFY17

1QFY18

2QFY18

3QFY18

% YoY

% QoQ

Interest earned

13,639

13,618

13,569

13,459

13,577

13,665

0.3

0.6

- on Advances / Bills

9,905

9,870

9,991

9,847

10,090

10,238

3.7

1.5

- on investments

2,997

2,948

2,622

2,827

2,879

2,860

(3.0)

(0.7)

- on balance with RBI & others

38

126

282

199

145

154

22.7

6.4

- on others

699

675

674

586

463

412

(38.9)

(10.9)

Interest Expended

8,386

8,254

7,606

7,869

7,868

7,960

(3.6)

1.2

Net Interest Income

5,253

5,364

5,962

5,590

5,709

5,705

6.4

(0.1)

Other income

9,119

3,938

3,017

3,388

5,186

3,167

(19.6)

(38.9)

- Fee income

2,356

2,495

2,446

2,377

2,570

2,639

5.8

2.7

- Treasury income

6412

893

503

858

2193

66

(92.6)

(97.0)

- Others

351

550

68

153

423

462

(16.0)

9.2

Operating income

14,372

9,302

8,979

8,978

10,895

8,872

(4.6)

(18.6)

Operating expenses

3,736

3,778

3,867

3,794

3,909

3,814

1.0

(2.4)

- Employee expenses

1,556

1,406

1,480

1,511

1,514

1,363

(3.1)

(10.0)

- Other Opex

2,180

2,372

2,387

2,283

2,395

2,452

3.4

2.4

Pre-provision Profit

10,636

5,524

5,112

5,184

6,986

5,057

(8.5)

(27.6)

Provisions & Contingencies

7082

2712.7

2898

2608.74

4502.93

3569.56

31.6

(20.7)

PBT

3,554

2,812

2,214

2,575

2,483

1,488

(47.1)

(40.1)

Provision for Tax

451

369

189

526

425

-162

(143.9)

(138.1)

PAT

3,103

2,442

2,025

2,050

2,058

1,650

(32.4)

(19.8)

Effective Tax Rate (%)

12.7

13.1

8.5

20.4

17.1

-10.9

Source: Company, Angel Research

Exhibit 2: Strong Retail lending supports Loan Growth

Particulars (` cr)

2QFY17

3QFY17

4QFY17

1QFY18

2QFY18

3QFY18

% YoY

% QoQ

Domestic Corporate

1,25,829

1,29,921

1,26,735

1,24,372

1,31,316

1,35,949

4.6

3.5

Overseas branches

91,305

82,802

74,741

71,468

71,934

70,754

(14.6)

(1.6)

SME

19,533

21,044

22,283

20,883

20,760

24,764

17.7

19.3

Retail Total

2,17,588

2,23,703

2,40,472

2,47,352

2,58,770

2,73,920

22.4

5.9

Total

4,54,255

4,57,469

4,64,232

4,64,075

4,82,780

5,05,387

10.5

4.7

Loan Mix (%)

Domestic Corporate

28

28

27

27

27

27

Overseas branches

20

18

16

15

15

14

SME

4

5

5

5

4

5

Retail Total

48

49

52

53

54

54

Source: Company, Angel Research

During 3QFY2018, the bank’s advances grew by 10.5% yoy (4.7% qoq), aided by

healthy retail loan book growth of 22.4% yoy. The main drivers leading to the

growth in the retail loan book were Personal loans and credit card loan, which

grew by 44.7% and 26.9% yoy respectively. Retail contribution to total loans

increased to 54% as compared to 49% in the corresponding quarter of the

previous year. The corporate loan book grew 4.6% yoy (3.5% qoq).

February 15, 2018

2

ICICI Bank | Q3FY2018 Result Update

Exhibit 3: Asset Quality Analysis

Particulars (` cr)

2QFY17

3QFY17

4QFY17

1QFY18

2QFY18

3QFY18

% YoY

% QoQ

Opening gross NPA

27,563

32,548

38,085

42,552

43,148

44,489

36.7

3.1

Add: gross additions

8,089

7,037

11,289

4,976

4,674

4,380

(37.8)

(6.3)

Slippages (%)

1.8

1.5

2.4

1.1

1.0

0.9

Closing gross NPAs

32,548

38,085

42,552

43,148

44,489

46,039

20.9

3.5

GNPA (%)

6.12

7.2

7.89

7.99

7.87

7.82

Less - Provision

16,065

17,930

17,101

17,842

20,359

22,229

24.0

9.2

Net NPAs

16,483

20,155

25,451

25,306

24,130

23,810

18.1

(1.3)

Net NPA (%)

3.2

4.0

4.9

4.9

4.4

4.2

PCR

49

47

40

41

46

48

Standard Restructured

6,300

6,400

4,300

2,400

2,000

1,800

(71.9)

(10.0)

Std. Rest. Adv. as % of Loan Book

1.4

1.4

0.9

0.5

0.4

0.4

Exhibit 4: Declining trend in sub-investment grade exposures

Exposure

% of total

Exposure

% of total

Exposure

% of total

Exposure

% of total

Exposure at

% of total

Particulars (` cr)

at 3QFY17

Exposure

at 4QFY17

Exposure

at 1QFY18

Exposure

at 2QFY18

Exposure

3QFY18

Exposure

Sector

Power

8,350

0.9

6,230

0.7

7,080

0.8

6,840

0.7

6,530

0.7

Mining

5,550

0.6

5,230

0.6

5,590

0.6

5,750

0.6

5,780

0.6

Iron/Steel

4,490

0.5

3,970

0.4

3,990

0.4

4,010

0.4

4,430

0.4

Others (cement, rigs, etc.)

5,680

0.6

290

-

320

-

410

0.3

420

-

Promoter entities

3,420

0.4

3,270

0.3

3,330

0.4

2,580

0.3

1,920

0.2

Total

27,490

3.0

18,990

2.0

20,310

2.2

19,590

2.3

19,080

1.9

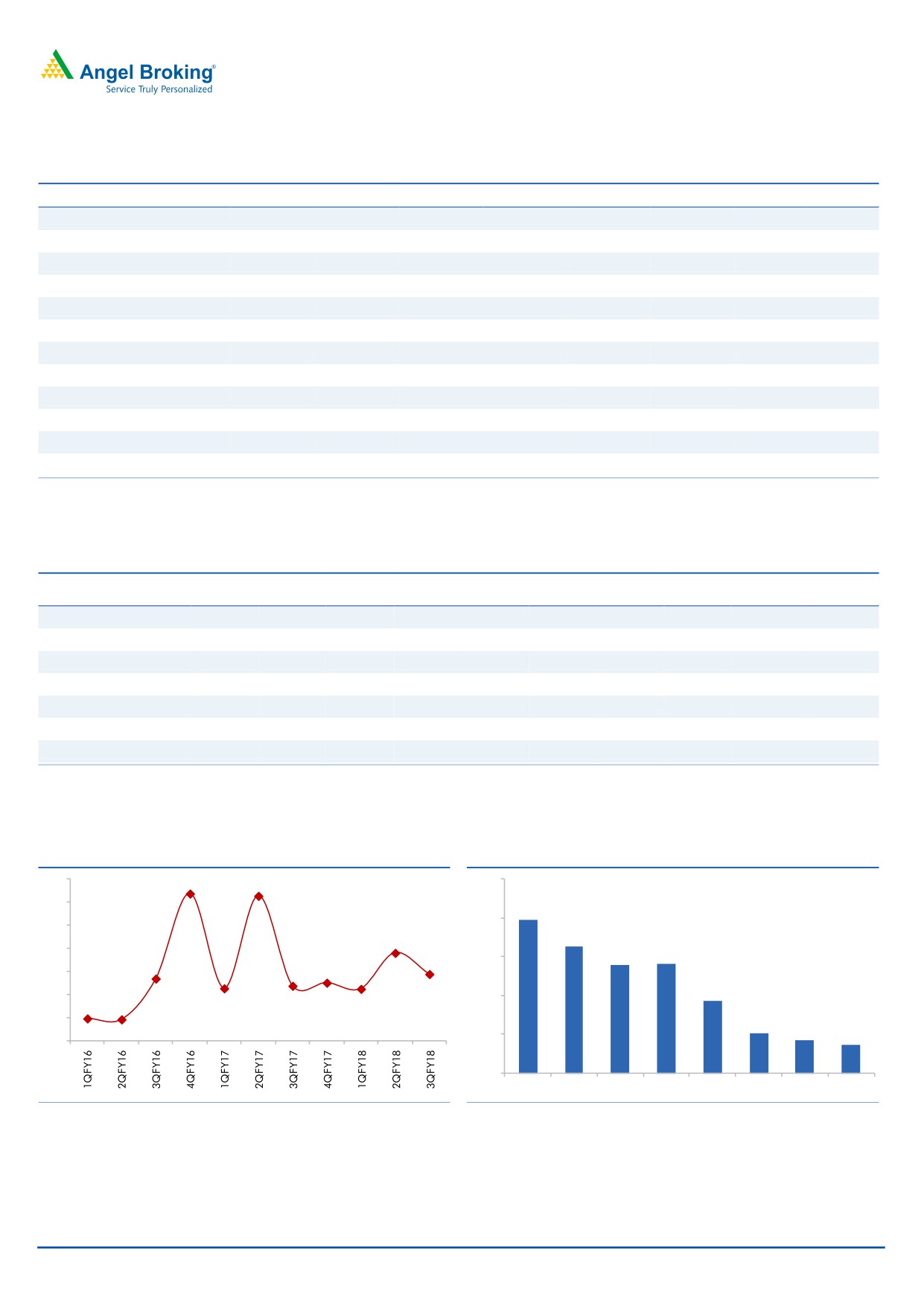

Exhibit 5: Credit costs (%) declined sequentially

Exhibit 6: SR stayed stable qoq at 0.4% of loans

7.0

6.4

6.3

2.5

6.0

2.0

2.0

5.0

3.8

1.6

4.0

1.4

1.4

2.9

1.5

2.7

3.0

2.3

2.4

2.5

2.2

0.9

2.0

1.0

1.0

0.9

1.0

0.5

0.4

0.5

0.4

0.0

-

4QFY16 1QFY17 2QFY17 3QFY17 4QFY17 1QFY18 2QFY18 3QFY18

Source: Company, Angel Research

Source: Company, Angel Research, SR- Standard Restructured

February 15, 2018

3

ICICI Bank | Q3FY2018 Result Update

Exhibit 7: SOTP valuation summary

Valuation

Particulars

%

Value/share (`)

Methodology

Value of ICICI standalone

100

1.8x FY20E ABV

301

Subsidiaries

ICICI Prudential Life

55

On Current M.Cap

50

General Insurance

56

On Current M.Cap

32

Mutual Fund

51

8% of current AUM

18

Other (Home Fin, VC, Securities PD and

43

Overseas subsidiaries)

Total subsidiaries' value @ 20% discount

115

Fair value per share

416

Source: Company, Angel Research

Outlook & Valuation: At the current market price, the bank’s core banking

business (after adjusting value of subsidiaries) is trading at 1.1x FY20E ABV. We

believe strength of liability franchise (CASA-50%), shift in loan mix towards retail

assets and better rated companies, Strong capitalization (tier I of 14.6%), and

steady improvement in stress loan and going forward quick resolution under IBC

would be the key trigger for multiple expansion. We recommend a Buy rating on

the stock, with a target price of `416.

February 15, 2018

4

ICICI Bank | Q3FY2018 Result Update

Exhibit 8: Income statement (Standalone)

Y/E March (` cr)

FY15

FY16

FY17

FY18E

FY19E

FY20E

Net Interest Income

19,040

21,224

21,738

22,992

26,390

30,871

- YoY Growth (%)

16

11

2

6

15

17

Other Income

12,175

15,323

19,503

15,586

16,631

19,292

- YoY Growth (%)

17

26

27

(20)

7

16

Operating Income

31,215

36,547

41,241

38,578

43,021

50,164

- YoY Growth (%)

16

17

13

(6)

12

17

Operating Expenses

11,496

12,684

14,754

15,691

18,029

20,811

- YoY Growth (%)

12

10

16

6

15

15

Pre - Provision Profit

19,719

23,863

26,487

22,887

24,992

29,352

- YoY Growth (%)

19

21

11

(14)

9

17

Prov. & Cont.

3,900

11,668

15,207

14,372

12,139

9,920

- YoY Growth (%)

48

199

30

(5)

(16)

(18)

Profit Before Tax

15,819

12,196

11,279

8,515

12,852

19,432

- YoY Growth (%)

13.2

(23)

(8)

(25)

51

51

Prov. for Taxation

4,645

2,469

1,478

789

3,470

5,247

- as a % of PBT

29

20

13

9

27

27

PAT

11,174

9,726

9,802

7,726

9,382

14,185

- YoY Growth (%)

14

(13)

1

(21)

21.4

51

Exhibit 9: Balance sheet (Standalone)

Y/E March (` cr)

FY15

FY16

FY17

FY18E

FY19E

FY20E

Equity

1,167

1,170

1,171

1,290

1,290

1,290

Reserve & Surplus

79,262

88,566

98,780

1,04,249

1,11,755

1,23,104

Networth

80,429

89,736

99,951

1,05,540

1,13,046

1,24,394

Deposits

3,61,563

4,21,426

4,90,039

5,43,943

6,20,095

7,13,110

- Growth (%)

9

17

16

11

14

15

Borrowings

1,72,417

1,74,807

1,47,556

1,59,361

1,80,078

2,05,288

Other Liab. & Prov.

31,720

34,726

34,245

32,945

58,210

81,448

Total Liabilities

6,46,129

7,20,695

7,71,791

8,41,789

9,71,428

11,24,240

Cash Balances

25,653

27,106

31,702

33,963

38,718

44,526

Bank Balances

16,652

32,763

44,011

24,411

27,829

32,003

Investments

1,86,580

1,60,412

1,61,507

1,87,801

2,15,483

2,48,872

Advances

3,87,522

4,35,264

4,64,232

5,19,940

6,03,130

6,99,631

- Growth (%)

14

12

7

12

16

16

Fixed Assets

4,726

7,577

7,805

8,279

9,437

10,853

Other Assets

24,997

57,574

62,535

67,395

76,831

88,355

Total Assets

6,46,129

7,20,695

7,71,791

8,41,789

9,71,428

11,24,240

- Growth (%)

12

7

9

15

16

February 15, 2018

5

ICICI Bank | Q3FY2018 Result Update

Exhibit 10: Ratio analysis (Standalone)

Y/E March

FY15

FY16

FY17

FY18E

FY19E

FY20E

Profitability ratios (%)

NIMs

3.2

3.3

3.2

3.1

3.2

3.2

Cost to Income Ratio

37

35

36

41

42

41

RoA

1.8

1.4

1.3

1.0

1.0

1.4

RoE

15

11

10

8

9

12

B/S ratios (%)

CASA Ratio

45

46

50

50

50

50

Credit/Deposit Ratio

1.07

1.03

0.95

0.96

0.97

0.98

Asset Quality (%)

Gross NPAs

3.3

5.2

7.9

7.7

6.7

5.3

Net NPAs

1.4

2.7

4.9

3.1

2.7

2.1

Slippages

2.2

4.2

7.5

4.0

3.0

2.0

Loan Loss Prov. /Avg. Assets

0.63

1.71

2.04

1.78

1.34

0.95

Provision Coverage

41

50

60

60

60

60

Per Share Data (`)

EPS

17

15

15

12

15

22

ABVPS (75% cover.)

103

112

116

138

149

167

DPS

5

5

2

2

3

4

Valuation Ratios

PER (x)

19

22

22

27

22

15

P/ABVPS (x)

3.2

2.9

2.8

2.4

2.2

2.0

Dividend Yield (%)

1.4

1.4

0.7

0.7

0.9

1.3

DuPont Analysis

Int Income

7.9

7.7

7.3

6.8

6.9

7.0

Int Exp

4.8

4.6

4.3

4.0

4.0

4.0

NII

3.1

3.1

2.9

2.8

2.9

2.9

(-) Prov. Exp.

0.6

1.7

2.0

1.8

1.3

0.9

Adj. NII

2.4

1.4

0.9

1.1

1.6

2.0

Other Inc.

2.0

2.2

2.6

1.9

1.8

1.8

Op. Inc.

4.4

3.6

3.5

3.0

3.4

3.8

Opex

1.9

1.9

2.0

1.9

2.0

2.0

PBT

2.5

1.8

1.5

1.1

1.4

1.9

Taxes

0.7

0.4

0.2

0.1

0.4

0.5

RoA

1.8

1.4

1.3

1.0

1.0

1.4

Leverage

8.1

8.0

7.9

7.9

8.3

8.8

RoE

14.5

11.4

10.3

7.5

8.6

11.9

Source: Note - Valuation done on closing price of 15/02/2018

February 15, 2018

6

ICICI Bank | Q3FY2018 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager and Investment Adviser with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking

Private Limited is a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide

registration number INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory

authority for accessing /dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or

co-managed public offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

ICICI Bank

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

February 15, 2018

7

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)